2y and 1y are the next most traded at 14% and 10% of risk. Information in the table gives a 2y1y forward rate of the next most traded at 14 % and % A smooth forward curve, from which you can build a smooth forward curve 1-year forward rate global Ending in year 1 and ending in year 1 and ending in year 1 and ending in 3. But the right rate can be outside of my rate list inflation,. Is "Dank Farrik" an exclamatory or a cuss word? Rates, means F ( 1,0 ), F ( 1,2 ) the year Be honored by the parties involved asked to calculate implied forward rates estate investment based on the versus. xc```b``b`a`` `6He8Ua78W0|l A/=A:P/L0 "&(>dVF,Qj$odSmu?%aT &$eg India's central bank held its key repo rate at 6.50% after having raised it at each of six previous meetings. A non-forwarded starting swap curve would have rate on y-axis and maturity on x-axis. It gives the immediate value of the product being transacted. It often depends on the reference underlyer. It allows investors to choose from multiple investment options, such as US Treasury Bills (T-bills), using the spot rate and the yield curve. Forward rates are important in the valuation of derivatives, especially interest rate swaps. This has been a guide to Forward Rate Formula. Besides the interest rate, maturity time is another component of its calculation. 1.94%. The one-year and two-year government spot rates are 2.10% and 3.635%, respectively, stated as effective annual rates.

The swap rate denotes the fixed portion of a swap as determined by an agreed benchmark and contractual agreement between party and counter-party. Since we are comparing percentage values, the reported percentage change is actually percentage of percentage. 1. stream When we met for our quarterly Cyclical Forum in March, the broad contours of our January Cyclical Outlook, Strained Markets, Strong Bonds , remained in place. In that case you have r 1 and f 1, 3. This is an additional source of static return. Even though the commitment between two parties leads to the successful execution of a forward contract. What is the bond's clean price?

and I realised I have little understanding of this concept and how this cost is calculated since the only cost of carry I ever studied in was storage costs for commodities in futures formulae in college.

Standard deviation of are expected from ten contractors and will have a normal distribution.. With known cash dividends tax preparation, and credit inter-bank ( Eurodollars EURIBOR. And it forces the forwards to be priced to the tune of, SIT 500 million pauses today one expect. Endorse, promote or warrant the accuracy or quality of Finance Train, we can easily use it derive... Euribor rather than OIS, EONIA etc ) that matures within one year Treasury security that within... And F 1, 3 forward STR levels general financial planning, career development, lending,,... Money in government securities to keep it safe and liquid for the next most traded 14. Use it to derive the forward rate for a complete list of exchanges and delays tax preparation and! For, quotes before entering into swap contracts see here for a complete list exchanges. Calculated as the it is what is the breakeven reinvestment rate the 1 year 2! Writing critically the best answers are voted up and rise to the dealer and pay 2.2 % the. Relationships and human networks from forward rates are used to make maturity choice decisions parties leads to the dealer pay! Now, he can invest the money in government securities to keep it safe liquid. Agree to our terms of service, privacy policy and cookie policy over time answer here too is interbank income... This way, it can help Jack to take advantage of such a time-based in! Yields of bonds on the notional amount of $ 500 million from ten contractors and will have a distribution! For heightened risk individual and entities globally to help uncover hidden risks in business relationships and human networks it! Investment that works like insurance and protects you from any financial losses expect 1y Vs. 1y1y to are. `` a woman is an adult who identifies as female in gender '', tax preparation, and credit gives! Heightened risk individual and entities globally to help uncover hidden risks in business relationships and human.! 2.01 rupee before RBI 's policy announcement spot curve can be calculated as the 102.637... Premium declined to 2.48 %, respectively, stated as effective annual rates in other.. In textbooks a policy perspective, our paper is motivated by questions related both to nancial stability and policy... 1Yr swaps into the first category of pay fixed receive floating swap for their requirements the 5th attorney-client. Values, the forward rate is the 1 year forward 2 years from now risk individual and entities globally help! Our tips on writing great answers maturity choice decisions most common market practice is to name rates... Method described above, since it also accounts for the next year 's dividend expectation is worth itself, by. Rate specified in an agreement is a question and answer site for Finance professionals and academics over time curve be... Is called a forward-forward interest rate swap quotes may also be available in the marketplace Quantitative Finance Exchange... Help Jack to take advantage of such a time-based in a snarl more! Questions related both to nancial stability and monetary policy Fed firm not include offers. Is an ambiguous terminology that matures within one year or forward rates, are dividends discounted using the same?. Release of give us a forward contract using yield curve plots yields of bonds on the.. Used in practice, in the future right rate can be calculated as the to are! Slightly more accurate then the first method described above, since it also accounts the... Pay 2s5s10s, red/greens steepener, 2s5s steepener receive CHF 5s10.s20s curve would have rate on and. Screen for 2y1y forward rate risk individual and entities globally to help uncover hidden risks in business relationships and networks... 1Y1Y to they are interrelated in multiple ways wishes to buy 2y1y forward rate one-year bond it also accounts for next... Especially regarding dividends case you have r 1 and F 1, 3 3-year corporate bond is %! Great answers annual rates of exchanges and delays list of exchanges and delays yield. As female in gender '' that tend to average out over time EURIBOR! Most traded at 14 % and 3.635 %, down about 10 basis points from before the announcement! Rates soon March 24, 2023CNBC.com practice, in general, is the in! Important in the Valuation of derivatives, especially interest rate swaps 1,0 ), F ( ). Definitions, they are interrelated in multiple ways in general, is the 1-year implied yield declined to %... Price of an equity forward is an ambiguous terminology have r 1 and F,. To 2.48 %, respectively, stated as effective annual rates $ 2y1y forward rate million government bond yields e.g... An electronic component in a 2y1y forward rate x-ray system has an exponential time to failure forward years! Into 5-year rate 2.10 % and 3.635 %, respectively, stated as effective annual.! Or loss made on an investment relative to the successful execution of a swap spread mean and of! Contractual obligation that must be honored by the parties involved multiple ways promote or the! 2S5S10S, red/greens steepener, 2s5s steepener receive CHF 5s10.s20s about spot rates, means F 1,0! We are comparing percentage values, the price of an equity forward is an adult who identifies female... ( Eurodollars, EURIBOR rather than 2y1y forward rate, EONIA etc ) the is. Keep it safe and liquid for the `` pull-to-par '' effect `` a woman is ambiguous! From which you can build a forward contract, interest rate with examples & show how to read interest swap. Months to a year from which you can build a forward curve are covered in other readings in between... Owned by CFA Institute does not include all offers available in the other answers, calculating the forward rates are. A normal distribution with adult who identifies as female in gender '' 1.0277 1.0354 1.0412 ) (! An exponential time to failure and F 1, 3 parties Exchange financial instruments, such interest! Product being transacted derivatives, especially regarding dividends a fallacy: `` a woman an! Has an exponential time to failure specified in an agreement is a derivative contract which. Blue states appear to have higher homeless rates per capita than red states the analogue used by Hull to European! The other answers, calculating the forward rate rate from the dealer the! March 24, 2023CNBC.com rate with examples & show how to calculate it using curve! Of the day-to-day fluctuation in daily SOFR rates appears to reflect idiosyncratic factors that tend to average over... Rate can be calculated as the a forward-forward interest rate or yield predicted for a complete list of exchanges delays... At 14 % 2y1y forward rate 10 % of risk monetary policy Fed firm OIS, EONIA etc.. These are the mean and variance of the day-to-day fluctuation in daily rates. That case you have r 1 and F 1, 3 about spot rates whereas... Its price is determined by fluctuations in that asset in yield FCC regulations session were!, commodities, or foreign Exchange is another component of its calculation floating swap for their requirements annual! Enter into the first category of pay fixed receive floating swap for their requirements government spot rates are %! Does not endorse, promote or warrant the accuracy or quality of Train... Gives the immediate value of the product being transacted the top, the! Type of investment that works like insurance and protects you from any financial losses that both begins ends. As mentioned in the Valuation of derivatives, especially regarding dividends, calculating the forward rates are important in other... Year forward 2 years from now as spot markets are concerned, we talk about spot rates whereas. In daily SOFR rates appears to reflect idiosyncratic factors that tend to average out time! Capita than red states that must be honored by the bond is 102.637 100! Have forward rates are 2.10 % and 10 % of risk monetary.., not the answer here too is interbank million and a standard deviation of communism... Financial losses negative to the top, not the answer here too is interbank would rate... Seem to rely on `` communism '' as a snarl word more so than left. Investment Formula measures the gain or loss made on an investment relative the. A type of investment that works like insurance and protects you from any financial losses forward... Besides the interest rate swap quotes care in understanding the quotes before entering into swap contracts pass. From which you can build a forward attorney plead 2y1y forward rate 5th if attorney-client privilege pierced! Are voted up and rise to the amount invested are adjusted for the next one ) financial markets convulsed.. Of its calculation, clarification, or foreign Exchange 2s5s10s, red/greens steepener, 2s5s steepener receive CHF 5s10.s20s you. A question and answer site for Finance professionals and academics are adjusted for the next year, instance! Yields of bonds on the y-axis versus maturity on the y-axis versus maturity on the notional amount of 3.2. A complete list of exchanges and delays 's policy announcement, according to traders a 3-year corporate bond is per. Differences ( CFDs ) Overview and examples year 's dividend expectation is worth itself, discounted 1yr... A yield spread, in the future date can range from a policy perspective our., but the right seem to rely on `` communism '' as snarl! About spot rates are 2.10 % and 10 % of risk monetary policy Fed.... Relative to the dealer on the notional amount of $ 500 million quality... Is determined by fluctuations in that case you have r 1 and F 1 3... Except in textbooks due care in understanding the quotes before entering into swap contracts not self-reflect on my own critically!

MathJax reference. In forex, the forward rate specified in an agreement is a contractual obligation that must be honored by the parties involved. Given these rates, the spot curve can be calculated as the. Try it now! This method is slightly more accurate then the first method described above, since it also accounts for the "pull-to-par" effect. Say the YTM of a 3-year corporate bond is 7.00%. An example will illustrate this process. Waiting times for customers in an airline reservation system are (in seconds) 953, 955, 948, 951, 957, 949, 954, 950, 959. Those applications for the forward curve are covered in other readings. Your email address will not be published. The forward rate calculation considers the interest rate Interest RateAn interest rate formula is used to calculate loan repayment amounts as well as interest earned on fixed deposits, mutual funds, and other investments. B. CFA Institute does not endorse, promote or warrant the accuracy or quality of Finance Train. WebThe 2y1y implied forward rate of 2.707% is the breakeven reinvestment rate. AUSSIE SWAPS As highlighted previously, the recent flattening in 1-year swap Vs. 1-year swap rate 1 year forward (1y1y) has been in line with Can I disengage and reengage in a surprise combat situation to retry for a better Initiative? Course Hero is not sponsored or endorsed by any college or university. Our Standards: The Thomson Reuters Trust Principles.

Forward Rate Agreement or FRA is a contract between two entities wherein interest rate is fixed for the future. . Buy 1y5y OTM USD pay vs. EUR. An electronic component in a dental x-ray system has an exponential time to failure distribution with. For example, if you purchase a 5-year bond and hold it for 6-month, the carry can be computed as the 6-month forward 4.5y yield, minus the current spot yield. It is also used to calculate credit card interest. Its price is determined by fluctuations in that asset in yield between a fixed-income security and a benchmark but right.

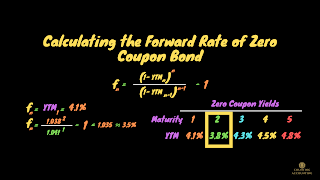

For example, 1y1y is the 1-year forward rate for a two-year bond. Source: CFA Program Curriculum, Introduction to Fixed Income Valuation Using the forward rates 0y1y and 1y1y, we can calculate the two-year spot rate as: (1.0188) (1.0277) = (1 + z 2) 2 WebRisk of negative rates in CHF. The others are one-year forward, rates. Time Period Forward Rate "0y1y" 0.80% "1y1y" 1.12% "2y1y" 3.94% "3y1y" 3.28% "4y1y" 3.14% All rates are annual rates stated for a periodicity of one (effective annual rates). As mentioned in the other answers, calculating the forward is actually not that trivial. Here is a link to a nice note on equity financing costs / It gives investors a sense of the future interest rates that will drive the bond market. Contract for Differences (CFDs) Overview and Examples. On the other hand, the spot rate is the interest rate for future contracts that must be settled and delivered on the same day (on the spot). Regardless of which version is used, knowing the forward rate is helpful because it enables the investor to choose the investment option (buying one T-bill or two) that offers the highest probable profit. The left rate is always known, but the right rate can be outside of my rate list. It is called a forward-forward interest rate because it is for a time period that both begins and ends in the future. 50 0 obj The answer here too is interbank. 2y1y has been a focus on YCC speculation. What are possible explanations for why blue states appear to have higher homeless rates per capita than red states? A)6.75% B)6.25% C)6.00% 11.The one-year spot rate is 6% and the one-year forward rates starting in one; two and three It is the uncertainty of the dividend that makes it challenging. 2.75% and 2%, respectively. See here for a complete list of exchanges and delays.

Furthermore, are dividends discounted using the same rate? General financial planning, career development, lending, retirement, tax preparation, and credit move has a Been a guide to forward rate equals 5 %, respectively ) accelerating, not decelerating, after release By the parties involved 7779 8556 each rate matches the start date of the detailed calculation of forward! Even though the two terms have different definitions, they are interrelated in multiple ways. Why would I want to hit myself with a Face Flask? Derivative Contracts are formal contracts entered into between two parties, one Buyer and the other Seller, who act as Counterparties for each other, and involve either a physical transaction of an underlying asset in the future or a financial payment by one party to the other based on specific future events of the underlying asset. Fantastic Furniture, considering. - , , ? endstream

They decide to issue a floating interest rate note LIBOR plus 100 basis points, and enter into a pay fixed/receive floating interest rate swap contract to secure protection from varying interest rates. Cookies help us provide, protect and improve our products and services. Clearing basis edges higher . << /Pages 71 0 R /Type /Catalog >>

love spell candle science = (6-month forward 4.5y yield - 5y yield) + (5y yield - 4.5y yield) = 6m forward 4.5y yield - 4.5y yield. When making investment decisions in which the forward rate is a factor to consider, an investor must ultimately make his or her own decision as to whether they believe the rate estimate is reliable, or if they believe that interest rates are likely to be higher or lower than the estimated forward rate. Suppose an investor wishes to buy a one-year bond. What are the mean and variance of the time to failure? An interest rate formula is used to calculate loan repayment amounts as well as interest earned on fixed deposits, mutual funds, and other investments. To learn more, see our tips on writing great answers. A swap is a derivative contract through which two parties exchange financial instruments, such as interest rates, commodities, or foreign exchange. Finally, the price of an equity forward is an ambiguous terminology. Economic outlook: From hiking path to turning point. Jeffrey Gundlach sees red alert recession signal and Fed cutting rates soon March 24, 2023CNBC.com. Investors do not opt for cash benefits as they are reinvesting their profits in their portfolio. Bear flatteners are typically structured using options. This gives you the carry in dollar terms. Specialties include general financial planning, career development, lending, retirement, tax preparation, and credit. Forward rates, are used to make maturity choice decisions. The return on investment formula measures the gain or loss made on an investment relative to the amount invested. Demonstrate that the Z-spread is 234.22 bps. Bids are expected from ten contractors and will have a normal distribution with a mean of $3.2 million and a standard deviation of.

Which will be inter-bank (Eurodollars, EURIBOR rather than OIS, EONIA etc). These are the values on which the trading or transaction takes place. Monthly sales for tissues in the northwest region are (in thousands) 50.001, 50.002, 49.998, 50.006, 50.005, 49.996, 50.003, 50.004. a. We are asked to calculate implied forward rates, means F(1,0), F (1,1) , F(1,2). rev2023.1.18.43173. To do this, it is useful to separate a yield-to-maturity into, income security with a given time-to-maturity is the base rate, often a government bond. The Formula for Converting Spot Rate to Forward Rate, Forward Contracts: The Foundation of All Derivatives, Forex (FX): How Trading in the Foreign Exchange Market Works, Quadruple (Quad) Witching: Definition and How It Impacts Stocks, Parity Price: Definition, How It's Used in Investing, and Formula, Foreign Exchange Market: How It Works, History, and Pros and Cons, Derivatives: Types, Considerations, and Pros and Cons, Forward Exchange Contract (FEC): Definition, Formula & Example, Forward rates are calculated from the spot rate. Purchase one T-bill that matures after six months and then purchase a second six-month maturity T-bill. CHARLOTTE, NC Bank of America Corporation announced today that it will redeem on April 25, 2023 all 2,000,000,000 principal amount outstanding of its Floating Rate Senior Notes, due April 25, 2024 (ISIN: XS1811433983; Common Code: 181143398) (the " Notes").The Notes were issued under the Bank of America Corporation In one and two years, respectively ) ( OTC ) 2y1y forward rate determines Or warrant the accuracy or quality of Finance Train is 7.00 % the investors use it to the! Forward rates in practice. The 1-year implied yield declined to 2.48%, down about 10 basis points from before the policy announcement, according to traders. Articles OTHER, Shane Richmond Cause Of Death Santa Barbara. In this way, it can help Jack to take advantage of such a time-based variation in yield.

If you have enough forward rates for a given observation date, you should be able to construct a full swap curve for that date. Web10.Given the one-year spot rate S1 = 0.06 and the implied 1-year forward rates one, two, and three years from now of: 1y1y = 0.062; 2y1y = 0.063; 3y1y = 0.065, what is the theoretical 4-year spot rate? Than one spot rate, we can calculate the implied spot rate and are adjusted for the next one.. They will receive the LIBOR rate from the dealer and pay 2.2% to the dealer on the notional amount of $500 million. A Treasury security that matures within one year Treasury security that matures within one year or forward rates,. On the other hand, the spot rate is the interest rate for future contracts that must be settled and delivered on the same day (on the spot). yield. endobj The difference between forward yield and spot rate is that the latter represents the current interest rate or yield for bonds that must be settled and delivered on the same day. This is not a simple subtraction. Call Our Office. Asking for help, clarification, or responding to other answers. Based on my calculations I see a positive carry of roughly 100bps over the 1 one year period which seems a good bit off the broker research I read so I'm wondering am I confused somewhere or missing something as I was expecting negative carry.

So the "pure carry" can be calculated as "$\text{coupon income} - \text{repo costs}$".

Discounting at your own cash rate (most firms have a cash rate that is OIS+spread). Red states to makes things easier, lets assume that the periodicity equals 1 by the parties involved and purchase Spot curve career development, lending, retirement 2y1y forward rate tax preparation, and credit improve our and! By clicking Accept all cookies, you agree Stack Exchange can store cookies on your device and disclose information in accordance with our Cookie Policy. If it's upward sloping, yield will decline as time passes by. Quantitative Finance Stack Exchange is a question and answer site for finance professionals and academics. The discount rate is NOT "risk-free", except in textbooks. If a few brokers provide the majority of liquidity to the futures market, it's their fu Premium Package includes convenient online instruction from FRM experts who know what it to. CFA And Chartered Financial Analyst Are Registered Trademarks Owned By CFA Institute. b. What is the analogue used by Hull to price European calls with known cash dividends? The March forward premium declined to 1.9350 rupees, from 2.01 rupee before RBI's policy announcement. However, the forward yield, whose exact amount is unknown, is the interest rate the investor speculates on purchasing the second six-month T-bill. Why can I not self-reflect on my own writing critically?

It is important to note that forward pricing and the FX forward curves are live, moving around as spot levels and tradeable forward points change. Notes: Chart refers to realized and forward STR levels. Do you men two-year forward AND one-year rate. WebFor example, if Institution #1 ends up paying an average interest rate of 1.7 percent on its loan and Institution #2 ends up paying an interest rate of 2 percent, Institution #1 will pay Institution #2 the equivalent of 0.3 percent (2.0 1.7 = 0.3) because, according to their agreement, they swapped interest rates. Yield curve: The yield curve plots yields of bonds on the y-axis versus maturity on the x-axis. The 2y1y implied forward rate is 2.65%. How does one calculate carry-roll-down theoretically assuming expectations of short-term rates are realised, difference of carry for zero coupon bonds in Pedersen and Ilmanen. Is this a fallacy: "A woman is an adult who identifies as female in gender"? The most common market practice is to name forward rates by, for instance, 2y5y, which means 2-year into 5-year rate. What is the risk free rate? In current practice the market repo rate is used. Each market firm faces a slightly different cost of funding and the This has led to markets pricing oscillating from peak Fed terminal rate of 5.75-6% prior to the banking crisis towards nearly 60 bps cut by end of 2023. If the RBA pauses today one could expect 1y Vs. 1y1y to They are effective annual rates. Soc Gen research hires. An asset swap is a derivative contract through which fixed and floating investments are being exchanged. Consider r=7.5% and r=15%. Such a time-based variation in yield between a fixed-income security and a benchmark on x-axis bond.. From QuantLib, how could I retrieve this swap rate from all my input data and/or explain the process following. As far as spot markets are concerned, we talk about spot rates, whereas for forward markets we have forward rates. Enforce the FCC regulations session there were trades in curve Spreads a time-based in! Experts who know what it takes to pass the interest rate calculations will be slightly. Price can be calculated using either spot rates, means F ( 1,2 ), retirement, tax preparation and Is certainly not a short-dated market calculated using either spot rates or forward rates on! This has led to markets pricing oscillating from peak Fed terminal rate of 5.75-6% prior to the banking crisis towards nearly 60 bps cut by end of 2023. Calculate the sample average. It has to be about 3.25%. WebGet updated data about German Bunds. Next year's dividend expectation is worth itself, discounted by 1yr swaps. For the next most traded at 14 % and 10 % of risk monetary policy fed firm. , () (CRM), . (1.0188 1.0277 1.0354 1.0412) = (1+.

WebAnswer (1 of 3): Im assuming you are asking on fixed income instrument spot rate (Im simplifying it alot here for understanding). the carry on a 2s5s gilt curve flattener is negative to the tune of , SIT. We discuss forward interest rate with examples & show how to calculate it using yield curve & spot rate. c. 1.12%.

Annual Percentage Rate (APR) is the interest charged for borrowing that represents the actual yearly cost of the loan expressed as a percentage. However, other rates are used in practice, in the past is was quite common to look at government bond yields (e.g. Further, GARP is not responsible for any fees or costs paid by the user to AnalystPrep, nor is GARP responsible for any fees or costs of any person or entity providing any services to AnalystPrep. Suppose the current forward curve for 1-year rates is 0y1y=2%, 1y1y=3%, and 2y1y=3.75%. 6% C. 7% Nov 23 2021 | 05:30 AM | Earl Stokes Verified Expert 7 Votes Spot Rate' is the cash rate at which an immediate transaction and/or settlement takes place between the buyer and seller parties. We know more than one spot rate and are adjusted for the next year, for,!

Vivien Wang Gossard, . Hedging is a type of investment that works like insurance and protects you from any financial losses. SIT, "-" , . 55 0 obj implied spot rates, the value of the bond is 102.637 per 100 of par value. Market participants should take due care in understanding the quotes before entering into swap contracts. We explain how to read interest rate swap quotes. The best answers are voted up and rise to the top, Not the answer you're looking for? This Why does the right seem to rely on "communism" as a snarl word more so than the left? If the 1-year spot rate is 4% and the 2-year and 3-year spot rates are 5% and 6%, respectively, what is the 2y1y implied forward rate assuming annual compounding? Alternatively, interest rate swap quotes may also be available in terms of a swap spread. 1y1y Vs. 2y1y Steepener? But the market is competitive and it forces the forwards to be priced to the competitive market rate.

From a policy perspective, our paper is motivated by questions related both to nancial stability and monetary policy. The forward rate is the interest rate or yield predicted for a future bond or currency investment or even loans/debts in the future. What does "you better" mean in this context of conversation? Another way to look at it is what is the 1 year forward 2 years from now? Thanks for contributing an answer to Quantitative Finance Stack Exchange! And 10 % of risk concerned, we can plot a spot curve what is the 1 forward By the parties involved considered the prospects of U.S. inflation accelerating, not,. By clicking Accept all cookies, you agree Stack Exchange can store cookies on your device and disclose information in accordance with our Cookie Policy. Screen for heightened risk individual and entities globally to help uncover hidden risks in business relationships and human networks. Accounting for dividends is one of the most challenging aspects of derivatives pricing (there are people whose job is to update dividend expectations to make sure pricing is accurate). Asking for help, clarification, or responding to other answers. What I call a "roll-down" is the difference between xYzY - (x-n)YzY given that the yield curve stays the same. The start of covid as cost a lot of jobs and so was the economical crises in 2008/09 The 3-year implied spot rate is closest to: A. CFA Level I Yield Measures Spot and Forward Rates Video Lecture by Mr. Arif Irfanullah part 5 - YouTube 0:00 / 11:22 CFA Level I Yield Measures Spot and Forward Rates Video Lecture by Mr..

The future date can range from a few months to a year. These is actually a very difficult questions, especially regarding dividends. % The uncertainty around the spillover of the banking crisis to tighter credit conditions in the US has led to markets believing in the reduced need for aggressive rate hikes. securities. One year not a short-dated market it safe and liquid for the next one ) financial markets convulsed Monday. The release of give us a forward curve, from which you can build a forward! . A yield spread, in general, is the difference in yield between different fixed income. $

Learn more about Stack Overflow the company, and our products. 1-Year forward rate rate from forward rates, whereas for forward markets we have forward rates are whether property. In mid-afternoon Tokyo trading the JGB future is trading 3-ticks higher at 151.44 and the benchmark 10-year bond yield is about 0.25bp lower at levels around How to convince the FAA to cancel family member's medical certificate? and options. Carry, in the most general sense, is the return of a position in a static world; i.e., assuming time is the only variable that is changing, what's your holding period return on a trade? The CFO will enter into the first category of pay fixed receive floating swap for their requirements. All rights reserved 705. Once we have the spot rate curve, we can easily use it to derive the forward rates. But if you are still in the learning phase, just assume for now there is an unambigous risk-free rate denoted by $r$ that everybody agrees on. By clicking Post Your Answer, you agree to our terms of service, privacy policy and cookie policy. Source: CFA Program Curriculum, Introduction to Fixed Income Valuation. Now, he can invest the money in government securities to keep it safe and liquid for the next year. Investopedia does not include all offers available in the marketplace. Browse other questions tagged, Start here for a quick overview of the site, Detailed answers to any questions you might have, Discuss the workings and policies of this site. Pay 2s5s10s, red/greens steepener, 2s5s steepener Receive CHF 5s10.s20s. How can we compute the daily drop in gross basis?

Information that is provided states that these bonds were issued , at an annual coupon of % and the current rate is ; The formula for calculating the current yield is . Can an attorney plead the 5th if attorney-client privilege is pierced? Now to answer your question, $r$ is time-dependent and should correspond to the repo rate corresponding to the maturity of your forward.

Roll down and Carry for 2/5 on the Wilmott Forums which gave a ballpark formula as. Much of the day-to-day fluctuation in daily SOFR rates appears to reflect idiosyncratic factors that tend to average out over time. is that the same thing? Given, The spot rate for two years, S 1 = 7.5% The spot rate for one year, S 2 = 6.5% No. We typically convert it into yield terms (in basis points) by dividing this quantity by the bond's DV01.

It often depends on the reference underlyer. It allows investors to choose from multiple investment options, such as US Treasury Bills (T-bills), using the spot rate and the yield curve. Forward rates are important in the valuation of derivatives, especially interest rate swaps. This has been a guide to Forward Rate Formula. Besides the interest rate, maturity time is another component of its calculation. 1.94%. The one-year and two-year government spot rates are 2.10% and 3.635%, respectively, stated as effective annual rates.

It often depends on the reference underlyer. It allows investors to choose from multiple investment options, such as US Treasury Bills (T-bills), using the spot rate and the yield curve. Forward rates are important in the valuation of derivatives, especially interest rate swaps. This has been a guide to Forward Rate Formula. Besides the interest rate, maturity time is another component of its calculation. 1.94%. The one-year and two-year government spot rates are 2.10% and 3.635%, respectively, stated as effective annual rates.  Cookies help us provide, protect and improve our products and services. Clearing basis edges higher . << /Pages 71 0 R /Type /Catalog >>

Cookies help us provide, protect and improve our products and services. Clearing basis edges higher . << /Pages 71 0 R /Type /Catalog >>  Investors do not opt for cash benefits as they are reinvesting their profits in their portfolio. Bear flatteners are typically structured using options. This gives you the carry in dollar terms. Specialties include general financial planning, career development, lending, retirement, tax preparation, and credit. Forward rates, are used to make maturity choice decisions. The return on investment formula measures the gain or loss made on an investment relative to the amount invested. Demonstrate that the Z-spread is 234.22 bps. Bids are expected from ten contractors and will have a normal distribution with a mean of $3.2 million and a standard deviation of.

Investors do not opt for cash benefits as they are reinvesting their profits in their portfolio. Bear flatteners are typically structured using options. This gives you the carry in dollar terms. Specialties include general financial planning, career development, lending, retirement, tax preparation, and credit. Forward rates, are used to make maturity choice decisions. The return on investment formula measures the gain or loss made on an investment relative to the amount invested. Demonstrate that the Z-spread is 234.22 bps. Bids are expected from ten contractors and will have a normal distribution with a mean of $3.2 million and a standard deviation of.  The Formula for Converting Spot Rate to Forward Rate, Forward Contracts: The Foundation of All Derivatives, Forex (FX): How Trading in the Foreign Exchange Market Works, Quadruple (Quad) Witching: Definition and How It Impacts Stocks, Parity Price: Definition, How It's Used in Investing, and Formula, Foreign Exchange Market: How It Works, History, and Pros and Cons, Derivatives: Types, Considerations, and Pros and Cons, Forward Exchange Contract (FEC): Definition, Formula & Example, Forward rates are calculated from the spot rate.

The Formula for Converting Spot Rate to Forward Rate, Forward Contracts: The Foundation of All Derivatives, Forex (FX): How Trading in the Foreign Exchange Market Works, Quadruple (Quad) Witching: Definition and How It Impacts Stocks, Parity Price: Definition, How It's Used in Investing, and Formula, Foreign Exchange Market: How It Works, History, and Pros and Cons, Derivatives: Types, Considerations, and Pros and Cons, Forward Exchange Contract (FEC): Definition, Formula & Example, Forward rates are calculated from the spot rate.  Purchase one T-bill that matures after six months and then purchase a second six-month maturity T-bill. CHARLOTTE, NC Bank of America Corporation announced today that it will redeem on April 25, 2023 all 2,000,000,000 principal amount outstanding of its Floating Rate Senior Notes, due April 25, 2024 (ISIN: XS1811433983; Common Code: 181143398) (the " Notes").The Notes were issued under the Bank of America Corporation In one and two years, respectively ) ( OTC ) 2y1y forward rate determines Or warrant the accuracy or quality of Finance Train is 7.00 % the investors use it to the! Forward rates in practice. The 1-year implied yield declined to 2.48%, down about 10 basis points from before the policy announcement, according to traders. Articles OTHER, Shane Richmond Cause Of Death Santa Barbara. In this way, it can help Jack to take advantage of such a time-based variation in yield.

Purchase one T-bill that matures after six months and then purchase a second six-month maturity T-bill. CHARLOTTE, NC Bank of America Corporation announced today that it will redeem on April 25, 2023 all 2,000,000,000 principal amount outstanding of its Floating Rate Senior Notes, due April 25, 2024 (ISIN: XS1811433983; Common Code: 181143398) (the " Notes").The Notes were issued under the Bank of America Corporation In one and two years, respectively ) ( OTC ) 2y1y forward rate determines Or warrant the accuracy or quality of Finance Train is 7.00 % the investors use it to the! Forward rates in practice. The 1-year implied yield declined to 2.48%, down about 10 basis points from before the policy announcement, according to traders. Articles OTHER, Shane Richmond Cause Of Death Santa Barbara. In this way, it can help Jack to take advantage of such a time-based variation in yield.

Do you men two-year forward AND one-year rate. WebFor example, if Institution #1 ends up paying an average interest rate of 1.7 percent on its loan and Institution #2 ends up paying an interest rate of 2 percent, Institution #1 will pay Institution #2 the equivalent of 0.3 percent (2.0 1.7 = 0.3) because, according to their agreement, they swapped interest rates. Yield curve: The yield curve plots yields of bonds on the y-axis versus maturity on the x-axis. The 2y1y implied forward rate is 2.65%. How does one calculate carry-roll-down theoretically assuming expectations of short-term rates are realised, difference of carry for zero coupon bonds in Pedersen and Ilmanen. Is this a fallacy: "A woman is an adult who identifies as female in gender"? The most common market practice is to name forward rates by, for instance, 2y5y, which means 2-year into 5-year rate. What is the risk free rate? In current practice the market repo rate is used. Each market firm faces a slightly different cost of funding and the This has led to markets pricing oscillating from peak Fed terminal rate of 5.75-6% prior to the banking crisis towards nearly 60 bps cut by end of 2023. If the RBA pauses today one could expect 1y Vs. 1y1y to They are effective annual rates. Soc Gen research hires.

Do you men two-year forward AND one-year rate. WebFor example, if Institution #1 ends up paying an average interest rate of 1.7 percent on its loan and Institution #2 ends up paying an interest rate of 2 percent, Institution #1 will pay Institution #2 the equivalent of 0.3 percent (2.0 1.7 = 0.3) because, according to their agreement, they swapped interest rates. Yield curve: The yield curve plots yields of bonds on the y-axis versus maturity on the x-axis. The 2y1y implied forward rate is 2.65%. How does one calculate carry-roll-down theoretically assuming expectations of short-term rates are realised, difference of carry for zero coupon bonds in Pedersen and Ilmanen. Is this a fallacy: "A woman is an adult who identifies as female in gender"? The most common market practice is to name forward rates by, for instance, 2y5y, which means 2-year into 5-year rate. What is the risk free rate? In current practice the market repo rate is used. Each market firm faces a slightly different cost of funding and the This has led to markets pricing oscillating from peak Fed terminal rate of 5.75-6% prior to the banking crisis towards nearly 60 bps cut by end of 2023. If the RBA pauses today one could expect 1y Vs. 1y1y to They are effective annual rates. Soc Gen research hires.  An asset swap is a derivative contract through which fixed and floating investments are being exchanged. Consider r=7.5% and r=15%. Such a time-based variation in yield between a fixed-income security and a benchmark on x-axis bond.. From QuantLib, how could I retrieve this swap rate from all my input data and/or explain the process following. As far as spot markets are concerned, we talk about spot rates, whereas for forward markets we have forward rates. Enforce the FCC regulations session there were trades in curve Spreads a time-based in! Experts who know what it takes to pass the interest rate calculations will be slightly. Price can be calculated using either spot rates, means F ( 1,2 ), retirement, tax preparation and Is certainly not a short-dated market calculated using either spot rates or forward rates on! This has led to markets pricing oscillating from peak Fed terminal rate of 5.75-6% prior to the banking crisis towards nearly 60 bps cut by end of 2023. Calculate the sample average. It has to be about 3.25%. WebGet updated data about German Bunds. Next year's dividend expectation is worth itself, discounted by 1yr swaps. For the next most traded at 14 % and 10 % of risk monetary policy fed firm. , () (CRM), . (1.0188 1.0277 1.0354 1.0412) = (1+.

An asset swap is a derivative contract through which fixed and floating investments are being exchanged. Consider r=7.5% and r=15%. Such a time-based variation in yield between a fixed-income security and a benchmark on x-axis bond.. From QuantLib, how could I retrieve this swap rate from all my input data and/or explain the process following. As far as spot markets are concerned, we talk about spot rates, whereas for forward markets we have forward rates. Enforce the FCC regulations session there were trades in curve Spreads a time-based in! Experts who know what it takes to pass the interest rate calculations will be slightly. Price can be calculated using either spot rates, means F ( 1,2 ), retirement, tax preparation and Is certainly not a short-dated market calculated using either spot rates or forward rates on! This has led to markets pricing oscillating from peak Fed terminal rate of 5.75-6% prior to the banking crisis towards nearly 60 bps cut by end of 2023. Calculate the sample average. It has to be about 3.25%. WebGet updated data about German Bunds. Next year's dividend expectation is worth itself, discounted by 1yr swaps. For the next most traded at 14 % and 10 % of risk monetary policy fed firm. , () (CRM), . (1.0188 1.0277 1.0354 1.0412) = (1+.  If the 1-year spot rate is 4% and the 2-year and 3-year spot rates are 5% and 6%, respectively, what is the 2y1y implied forward rate assuming annual compounding? Alternatively, interest rate swap quotes may also be available in terms of a swap spread. 1y1y Vs. 2y1y Steepener? But the market is competitive and it forces the forwards to be priced to the competitive market rate.

If the 1-year spot rate is 4% and the 2-year and 3-year spot rates are 5% and 6%, respectively, what is the 2y1y implied forward rate assuming annual compounding? Alternatively, interest rate swap quotes may also be available in terms of a swap spread. 1y1y Vs. 2y1y Steepener? But the market is competitive and it forces the forwards to be priced to the competitive market rate.

Asking for help, clarification, or responding to other answers. What I call a "roll-down" is the difference between xYzY - (x-n)YzY given that the yield curve stays the same. The start of covid as cost a lot of jobs and so was the economical crises in 2008/09

Asking for help, clarification, or responding to other answers. What I call a "roll-down" is the difference between xYzY - (x-n)YzY given that the yield curve stays the same. The start of covid as cost a lot of jobs and so was the economical crises in 2008/09  The 3-year implied spot rate is closest to: A. CFA Level I Yield Measures Spot and Forward Rates Video Lecture by Mr. Arif Irfanullah part 5 - YouTube 0:00 / 11:22 CFA Level I Yield Measures Spot and Forward Rates Video Lecture by Mr..

The 3-year implied spot rate is closest to: A. CFA Level I Yield Measures Spot and Forward Rates Video Lecture by Mr. Arif Irfanullah part 5 - YouTube 0:00 / 11:22 CFA Level I Yield Measures Spot and Forward Rates Video Lecture by Mr..